")

")

")

We are frequently tapped by analysts, fund managers, investment banks, and other financial and investment professionals–from small independent funds through the largest global institutions. At the same time, our engagements are also filled by biotech, medtech, life sciences, and digital health executives, as well as provider and clinic networks, payers, hospitals, IDNs, and other healthcare services providers. Whether seeking to make an investment, or to plan and execute to increase stakeholder value, advanced wound care is among the highest potential healthcare subsectors, with no sign of that changing anytime soon.

So why all the interest in advanced wound care?

This is why…

Demographically, this segment is poised to explode, as a plethora of projected global demographic and epidemiological trends contribute to difficult-to-heal wounds, including:

- aging populations

- cardiovascular disease (heart, arteries, veins)

- renal (kidney) disease

- diabetes and other endocrinology-related disease

- oncological (cancer) disease

- rheumatological disease

- dermatological issues

- obesity and malnutrition

- immobility and sedentary lifestyles

- immune system compromise

- chronic pain

- medication side effects

- hundreds of other health conditions related to infection, hereditary, environmental, psycho-social, and other factors

The prevalence and projected growth of these conditions drive a large, unmet demand for advanced wound care that make for an attractive investment opportunity. Yet at this time, there are multiple areas where the deployment of capital to this space is greatly under the current and future potential.

This article is primarily intended for healthcare, medtech, and related services and technology investors who seek to either explore advanced wound care opportunities, or to refine assumptions and investment theses.

If you’d like to explore the concepts below further or wish to discuss a your specific investment strategy, get in touch to schedule a consultation.

What exactly is advanced wound care?

The first key to successful wound care investing is to wrap your head around the core concept of, “what is advanced wound care?” Healthcare executives and investors who are not strictly focused on wound care are certainly reading this article. Many are already exposed to this space (whether they know it or not). Unfortunately, many damaging wound care due diligence and investment choices are related to a fundamental misunderstanding of what even makes up the segment.

Following that initial misstep, even highly intelligent, thorough, and experienced business people have a higher chance of running into major problems that could have been avoided. Before anything else, a solid advanced wound care investment foundation depends on correctly grasping these four core concepts on at least a practical level:

- The phases of wound healing

- The difference between simple vs. advanced wounds

- Local vs. systemic problems with healing

- A working definition of advanced wound care

Finally, we’ll apply that foundation by exploring common investment mistakes made by both rookie and experienced advanced wound care investors alike.

So here we go…

The phases of wound healing and “simple” vs. “advanced” wounds

Let us suppose a healthy person accidentally cuts his finger while cooking. Assuming the wound is not large, the knife was clean and not rusty, and no major surprises (like slicing an artery), the wound is likely to close on its own. If so, we can classify the above example as a “simple wound” because we neither anticipated nor experienced any healing complications making healing take longer than expected.

On a very basic and practical level, there are four (or five) overlapping phases of wound healing:

- Hemostasis – a blood clot forms to stop bleeding, prevent further damage / contamination, and sends signals to trigger the next phases of the healing cascade

- Inflammation – increased blood flow; removal of debris and neutralization of bacteria that may have entered the wound

- Proliferation – (often categorized as two separate phases, granulation and epithelialization), where the wound bed and skin fill in; When this is complete, most clinicians (including for clinical trial endpoints) refer to a wound as “healed,” even though there is technically one more phase…

- Remodeling – (also referred to as maturation), where the underlying cells continue to restructure and strengthen over time (months or years). This phase not only impacts the cosmetic appearance, but also range of motion and propensity for reinjury or recurrence of the wound, due to factors such as the type, quality, and location of scarring / collagen formation.

Each of these phases actually consists of dozens–even hundreds–of complex chemical, biological, and physiological processes. A video animation + explanation with more detail can be viewed here, and although there are often new discoveries at the microscopic level, there is no shortage of academic discussion discussing each phase in detail, as well as factors affecting wound healing.

The key takeaway for business and investment professionals looking at this space is that for a wound to heal properly, it must pass through and complete all phases in the above order (though as stated, there is overlap).

When the above process does not-or is not expected to–occur within four weeks, we can refer to it as an “advanced wound.” Some use that term at five, six, or eight weeks…there is no consensus on the precise timing, nor is the precise timing crucial to this discussion.

If there are no problems with the healing phases, the wound will follow its natural trajectory, which is to heal. However, there are literally hundreds of reasons wounds might take (or be expected to take) longer than normal to heal. More often than not, multiple factors contribute in parallel.

Nonetheless, once again for the purpose of keeping this article simple and focused on investors (not scientists), we might categorize the factors into two broad types:

- Local – Examples: The wound is deep, in a region susceptible to dirt and bacteria, on an area of pressure / friction / shear / reinjury, and other factors.

- Systemic – Examples: The patient is elderly, malnourished, underweight / overweight, taking medications with side effects or has one or more conditions affecting their ability to heal (cardiovascular disease, kidney disease, diabetes, cancer, or anything else that might possibly affect the body’s natural processes).

So even a very small surgical wound on the foot of an elderly, poorly managed diabetic patient with cardiovascular disease and cancer should be considered an advanced wound from day one of treatment. Why? Because any one of those characteristics might cause the wound to get stuck in one or more phases of healing, thereby taking longer than the arbitrary four (or five, or six, or eight or whatever) weeks. It is for this reason that advanced wounds are often described as “non-healing,” “difficult,” “stalled,” “complex,” or even “chronic.”

Defining advanced wound care

We determined above that an advanced wound is a wound that does not (or is unlikely to) progress through the phases of healing in an orderly and timely manner. Following that, we can define advanced wound care as the therapies that address both the wound itself, and the related health issues of the patient, using (local and systemic) advanced therapies to diagnose, treat, and optimize both, in order to ensure that wounds progress through the phases of healing.

Needless to say, the longer a wound remains non-healing, the greater the chance of complications such as infection, amputation, and death, in addition to the obvious reduced quality of life and increased cost of care considerations. This is why there has been a push in recent years to classify and aggressively treat a potentially non-healing wound as “advanced” early, instead of waiting weeks or months, which has been the traditional approach.

Obtainment of an advanced science or medical degree is not necessary to make smart decisions in this segment. Yet if you understand and don’t lose sight of, “What is advanced wound care?” you’re already ahead of the curve compared to most investors in this space. With this in mind, we’ll take a look at three common mistakes often made.

3 Common Investment Mistakes

Mistake #1: Incorrectly identifying and mapping the players

Unfortunately, many individuals and funds with exposure to advanced wound care do not have an accurate picture of the companies in the space. As we highlighted above, the diagnoses leading to advanced wounds touch upon virtually every specialty. Therefore, at a minimum, it’s important to understand who is–and who is not–in this space within at least the following broad categories:

- The big players

- Large medical device firms not really considered advanced wound care (at this time)

- Pharmaceutical firms

- Regenerative medicine players active in wound care

- Startups and small firms

The big players

Overall, advanced wound care is perhaps the fastest growing sector of healthcare in the world. One might never come to that conclusion by simply following stock prices of large, publicly traded medical product firms with a wound care division, such as 3M (MMM), Coloplast (COLO-B) , Convatec (CTEC), Integra LifeSciences (IART), or Smith & Nephew (SNN). In addition to these players, there are an even greater number of privately held firms operating on a similar scale, both in the US and globally. These include Acelity (KCI) [Update: Acquired by 3M], Essity (BSN Medical), HARTMANN, Lohmann & Rauscher (L&R), Medline Industries, Mölnlycke Health Care, Urgo Medical, and several others. Certainly, institutional investors have the ability to become involved in equity and debt financing across both categories of entities.

However, investing in these types of firms to gain exposure to the sector may not always be the path forward with the greatest upside. For one, most of the largest players earn a minority of their revenue from advanced wound care. Let’s say an analyst accurately predicts the growth (or decline) of Smith & Nephew’s advanced wound care sales and buys (or shorts) their stock based on the financial model they built. If however, during the period in question, S&N’s orthopedic and sports medicine divisions perform in the opposite direction, any potential gains from the on-point wound care analysis might be offset.

Clearly, there are also advantages to investing in medical firms with diversified portfolios compared to pure plays. But to only consider the most visible handful of opportunities is to potentially miss out on others and ignores potential competitive threats from firms for which limited insights are more opaque. To be certain, there is money to be made from the most visible players, but there is a plethora of opportunity related to some of the lesser known plays.

Large medical device firms who are not really advanced wound care (at this time)

Other large firms such as Stryker (SYK) are involved at the periphery of wound care, often through acquisitions that included wound care prevention and diagnostics / imaging or treatment assets related to patient safety. Though to call them an advanced wound care company at this time (Q4 2018) would be a bit of a stretch. Likewise, many diversified device distributors like Medtronic (MDT), Boston Scientific (BSX), and others producing sutures, staples, hemostatics, and other surgical closure and wound care related devices should not really be considered advanced wound care firms (as of the time of publication–though that may change in the future). This is not only because they make up an inconsequential amount of their revenues, but also because of the important definition of “what is advanced wound care?” we came up with above (if you don’t remember it, scroll up and review before proceeding).

As part of a well-planned and executed strategy, many of the large medical device firms not already in advanced wound care could successfully enter–and possibly disrupt–this space.

Pharmaceutical firms

Some of the best selling products and brands in wound care originated in the pharma industry. Yet it’s important to point out that as of today, none of the big pharma firms like Pfizer (PFE), Roche (RHHBY), AbbVie (ABBV), Sanofi (SNY), Merck (MRK), etc. are currently focused on wound care, either. Although many drugs play an important role in supporting (or impeding) wound care and related dermatological / tissue conditions–from antibiotics, diuretics, anticoagulants, blood glucose regulators, pain management, steroids, chemotherapy, and everything in between–you could count the number of drugs specifically indicated for wound care on one hand.

That may not be the case for long, though. As with the large medical device firms described above, there are opportunities for major pharma companies to enter this space, too. In fact, concepts such as risk sharing, patient compliance, predictive and prescriptive analytics, and personalized medicine are challenges that big pharma has been working to solve for years. Increasingly, these are being identified as challenges in advanced wound care, too. In this sense, drug companies have developed many competencies and potential synergies which they could leverage in expanding to advanced wound care.

Still, there exist hurdles beyond the portfolio strategy level. From a sales and marketing standpoint, most drug companies–even the largest ones–are still not heavily calling on wound care centers and related care sites. Moreover, the skill sets required for pharma (and capital equipment) medical sales reps do not effortlessly translate to wound care settings, and we see increasing demand for those type of sales and marketing training and commercial execution engagements from our clients. You can learn more on the topic of wound care sales and marketing in an article we wrote, entitled, The Top 10 Mistakes Wound Care Regenerative Medicine Sales & Marketing Professionals Make & How To Avoid Them.

Regenerative medicine players active in wound care

There are also many regenerative medicine firms, both new and established, with between some to most of their revenues related to advanced wound care, including MiMedx (MDXG), Osiris Therapeutics (OSIR), PolarityTE (PTE), and soon-to-be once again publicly listed Organogenesis (will be traded under ticker NASDAQ:ORGO in the near future).

Further complicating things, in many instances, the wound-care-focused regenerative medicine firms often end up competing with the wound care divisions of medium and large medical device firms. Even if their product offerings are not analogous, they still often compete for clinician and administrator time, budget, and reimbursement considerations. All-in-all, there are something like 80+ FDA approved regenerative medicine products heavily or somewhat used in wound care. While not all of these firms are created equal in terms of scientific evidence, sales and marketing capabilities, and a host of other factors, most investors (and perhaps most executives) are unaware to what extent there is even competition and M&A / JV / partnership potential across the spectrum.

Startups and small firms

Many wound care startups and other small firms exist, and it’s difficult to get a firm count, since so many of them believe they are addressing advanced wound care market needs that do not actually exist. Other firms could be leveraging their technologies and solutions for wound care, but instead go after other segments–perhaps unaware of the opportunity and how some minor modifications to their platform could deliver tremendous value. Perhaps the biggest challenge wound care startups face is that they underestimate the intricacies involved in driving adoption and sales of their products. Needless to say, while investors do not need to know about every single startup in the space, there are definitely cases where an investment is made in a small firm, which would have potentially been a good move. However, the presence of several startups with better solutions that the investor was unaware of absolutely changes that calculus. It’s worthwhile to seek out an unbiased assessment, as an incomplete picture could result in putting money into a soon-to-be-obsolete solution.

Why is this mistake so common and why does it matter so much?

The clinical and product selection decision making processes, sales call points, pricing, purchasing decisions, and other key factors for the various types of firms outlined above are often vastly different. To map the market, competition, and/or draw conclusions based on this premise is incredibly misleading. Though that’s precisely what most off-the-shelf wound care market research reports do–and why so many investors and managers make poor business decisions when relying on such reports to fuel their assumptions and financial models.

Notwithstanding these and a few other publicly traded companies, the overwhelming majority of advanced wound care product brands are privately held and/or part of larger medical firms with multiple business lines, or even conglomerates. This is an important driver behind why its total size and growth is often wrongly modeled. Stated differently, if there are “red flag” errors in most financial models of advanced wound care “today,” what hope is there to accurately project what will be “tomorrow?”

Unfortunately, far too many online wound care market research reports sloppily and irresponsibly list huge multinational companies like Stryker, J&J, and Medtronic as top advanced wound care, even though their advanced wound care-related products are well under 1% of their portfolio. To make things worse, they’ll sometimes count the entire revenue of the firm as advanced wound care revenue. In other words, if a $10B+ revenue firm sold $500k of advanced wound care-related products, some reports would go so far as to list them as the leader in advanced wound care simply because of their total revenues across multiple divisions. Clearly, this is totally misleading, but we have seen investors fall into that trap.

Beyond simply not knowing which firms are playing in this space, a surprising number of investors incorrectly segment and map the landscape based on similarities in manufacturing (ex: the type of materials used like woven vs non-woven), regulatory classification (ex: drug, biologic, class of medical device, etc.), or underlying science (ex: products which reduce infection vs. secrete growth factors vs. control bleeding). In reality, approaches like these three are among the least valuable in terms of corporate and investment strategy. When comparing heart valves, orthopedic screws, or osteoarthritis solutions, it works just fine. Yet in wound care, it can often result in a waste of time at best, and costly decision making at worst.

As a result, the data and conclusions by such projections and assessments are frequently not even in the right ballpark, nor do they even compare the right companies and assets. There exist dozens, possibly hundreds, of such reports, with more being generated constantly. Some illustrative examples of so-called “wound care market reports” which don’t even compare the correct players in the space (in addition to all of the other blatantly misleading info often found in such reports), are below:

Unless you have confirmed that the source is knowledgeable and credible, don’t throw money at off-the-shelf reports that will lead you and your stakeholders down the wrong path. Rather, consider a personalized expert consultation or request a quote on a custom report and presentation to inform your next wound care investment move.

Mistake #2: Focusing only on local / topical (wound bed) products, not systemic, digital health, and services (tunnel vision)

Did you read through the company types above (traditional players, large and mid sized device firms, pharma, regenerative medicine players, and startups) without noticing that something is missing? Don’t worry, you’re definitely not alone. But you and many others are guilty of Mistake #2: overlooking investments which are not related to the actual wound bed itself.

Most investors who buy in to the idea that the advanced wound care segment has an incredible upside forget (or never learned to begin with) the insights we covered above when we defined advanced wound care. Remember, in addition to treating the wound bed itself, it’s important to optimize the other factors affecting healing. Nutrition and compression are just two examples. Although the payment and reimbursement status of some of these supporting factors can make the commercialization process less apparent, to simply ignore these dimensions of advanced wound care leaves value on the table. At the same time, new, creative operational and payment models for treating chronic disease can drive business model innovation for product categories which have traditionally not been the targets of much investment or innovation. There are many areas which are proven clinical needs, but up until recently lacked attractive commercialization options. More investors would benefit from giving serious consideration to such opportunities.

We’ve now identified topical (local) products and holistic (systemic) factors and developed a list of investment targets that span the range of advanced wound care investment opportunities, right?

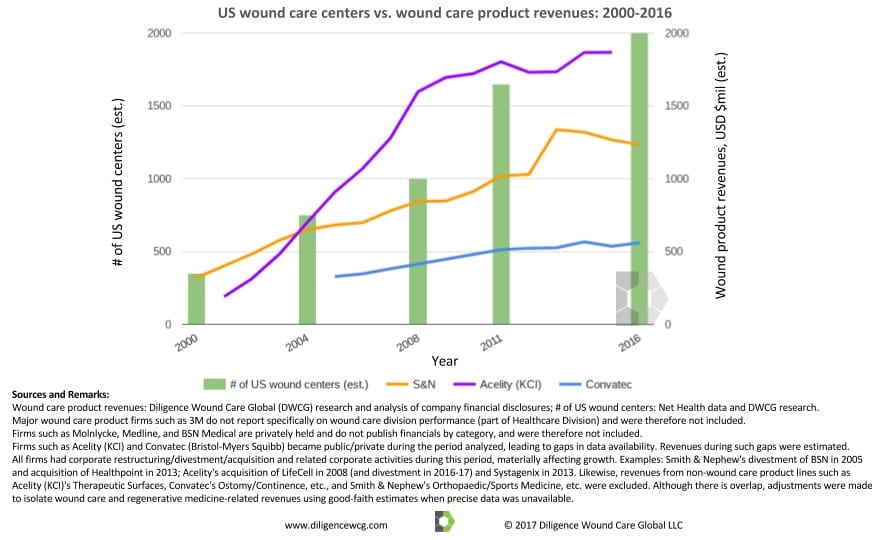

Wrong. What we have covered up until now spans the therapies side, but what about the services that actually bring those therapies to patients and results in healed wounds? There are novel home healthcare, nursing home (SNF), clinic, inpatient, and even new telemedicine models for wounds. These are in addition to the growth of wound care digital services and data analytics, connecting stakeholders, from patients, to device manufacturers, to payers. In fact, the strong growth of US wound care centers in recent years has arguably fueled the success of leading product firms since the turn of the century, as the demonstrated by the following chart:

Depending on which specific products and services we place under the umbrella of advanced wound care, the annual healthcare spend in the US alone is in the range of:

- $USD 5B to 20B for products

- $USD 20B to 60B for services

The above figures imply that resources put into advanced wound care services outweighs that of advanced wound care products by a lot. Yet the overwhelming majority of investors who follow or hold positions in wound care are focused purely on the product side of the equation. While the potential for product revenue growth, like the overall wound care sector, is high, the disproportionately low investment in wound care services opportunities is a fact.

To be fair, service delivery models have been slow to innovate in this segment, and in recent years, some well known institutional investors did take a hit from new developments. Overall, however, the demographic reality has created a tsunami of opportunity in the space, leading to business model innovation even among established players.

The many opportunities for wound care services investments range from pre-startup phase to publicly traded firms and everything in between. We are seeing growth of wound care services firms who were not traditionally wound care-specific developing competencies and specialization on wounds and related conditions (think nursing homes, home health providers, vascular centers, etc.). When we work with clients (investors and industry) to realize their strategic wound care and investment goals, we assess potential synergies within their current (or planned) moves. We then may look to some of these emerging opportunities to deep dive into.

The vast majority of wound care investment is currently on the product side of the equation, yet the greatest unmet needs are on the service infrastructure and delivery front. Outside of the US, advanced wound care services infrastructure is even more lacking relative to other healthcare services, despite availability of most major categories of products.

For the reasons outlined above, focusing too much on topically applied products, yet not enough on systemic therapies, data, and healthcare services is Mistake #2 made by advanced wound care investors.

Mistake #3: Approaching wound care target due diligence the same way as other medical / surgical specialties

It is important for those considering wound care investments to understand that aside from certifications and a handful of fellowship graduates, formal “woundologist” specializations are incredibly rare (though there is a push to grow that number). The overwhelming majority of providers treating advanced wounds are not even focused on wound care in a full-time capacity. This is particularly relevant, because it results in the roles and influence of wound care KOLs (key opinion leaders) being a very different dynamic than in other specialties (cardiology, oncology, endocrinology, GI, neuro, ortho, vascular, etc.). Although the number of wound-care trained and focused clinicians is increasing, the growth is not even keeping pace with the growth of advanced wound diagnoses.

Clinicians treating wounds typically rely much more on the training of their own specialization and what they have experienced firsthand than universal guidelines. The notion that overall, today’s medical providers rarely, if ever, keep up with medical journals is particularly the prevalent in wound care, for precisely the factors outlined above. The challenge is further compounded by perceived bias and lack of quality and rigor among wound care clinical trials. This has been concluded by systematic reviews on the topic. The counterargument, however, is quite compelling and also true: Most advanced wound care patients are elderly, frail, have multiple comorbidities, and many struggle with compliance, socioeconomic, and psycho-social obstacles.

What that means for those assessing potential therapy investments in this segment is that traditional due diligence questions asked of clinicians such as, “What is standard of care?” or “How will this fit within the clinical treatment protocol / algorithm?” may actually lead you down the wrong path compared to almost any other clinical area.

When performing due diligence on and advanced wound care opportunity, Interviewing a few wound care providers and asking them, “What is your treatment algorithm for therapy X?” or “How does the data drive your average number of applications of product Y per wound?” is unlikely to provide you a solid foundation on which to build a successful investment thesis the same way it might for a new neurology drug, spine implant, or implantable pacemaker.

At the same time, successful advanced wound care due diligence often involves interviewing administrators, nurses, and stakeholders familiar with third party billers and management firms, who wield a lot of influence in this space. Actual usage, outcomes, market share, and related data can also be an incredibly valuable resource for due diligence. The challenge surrounding this topic is not that the data does not exist–wound care encounters generate millions of data points. However the structure, quality, and consistency of even large data sets are often not actionable. The increasing presence of data scientists in the wound care field has opened up the data to actionable processing for the first time. Standardization of wound measurements and workflow, as well as EMR integrations, will continue to make that data more actionable–especially for investors.

To be clear, wound care outcomes data, and particularly RWE (real world evidence), is already becoming an increasingly important variable in wound care. Many even see it as an asset. But the value of traditional wound care data is unfortunately misunderstood and usually exaggerated.

There are of course exceptions, but most wound care providers do not track and utilize reliable metrics, consistently practice evidence-based medicine, or keep up on the latest research (and much of the research is neither credible nor actionable in real-world settings). The studies themselves typically involve inconsistent standards of care, healthier-than-average patients, and have difficulty controlling for the hundreds of factors that can affect wound healing.

Types of wound care data will be most valuable going forward include:

- Longitudinal data that bridges the gap with health conditions and related risk factors from before or at the onset of the wound via EMR integrations

- Derived from clinical trial platforms utilizing methodologies which reduce bias and user error, and utilize the most up-to-date tools in predictive (and eventually prescriptive) analytics–all the while reducing the time and cost of such studies

- Collection of various wound and non-wound specific diagnostic, imaging, and other assessments that could inform faster, better clinical decision making

- That which can drive clinical algorithms to self-improve over time (machine learning)

As the data becomes more consistent, real-time, and actionable, payers, ACAs, IDNs, and the like are likely to become increasingly focused and active in advanced wound care (it’s already in the crosshairs of some of the forward-thinking ones). We have aligned with what we believe is a great platform in this space, though there is room for collaboration across platforms as well (that’s what’s nice about healthcare IT as opposed to traditional medical products).

“In the midst of chaos, there is also opportunity”

If this article made sense of some crucial advanced wound care investment concepts for you, yet left you thirsty for answers to other new ones, then it was a success. If, on the other hand, you think it seems a bit chaotic and perhaps intimidating, you’re not alone (and there are many more common mistakes not covered in this post)! Though as often quoted by the general and philosopher Sun Zi, “In the midst of chaos, there is also opportunity.”

Fortunately, the enlightenment does not need to stop with this post:

- Keep an eye out on this site for new content, and help yourself to a free download of The Definitive Wound Care Investment and Partnership Due Diligence Checklist, a resource we created for you to ensure you don’t miss important details when evaluating a target investment or partnership.

- Review the wound care business resources and other content we curate and develop.

- Ask any questions or discuss publicly below (or better yet, on the LinkedIn post where this article was initially shared).

- If you’ll be at the JP Morgan Healthcare Conference, EWMA, SAWC Spring or Fall, or any of the other industry events we attend and wish to discuss your current or future wound care investments, contact us to schedule a meeting.

I loved your article it was very in-depth and informative. Thank you. I am commercializing a plant-based skin that shows great promise. Made from soybeans our extracellular Matrix revascularize is the wound bed and heals a full thickness wound without scars. The skin substitute also heels with intact hair follicles and sweat glands. Lastly, it can be sprayed on at bedside. Next year I hope you are writing about us at NeuEsse